No Results Found

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Every year we observe March 8 as International Women’s Day. According to the Unite Nations, the purpose of this day is to uphold women’s achievements, recognize challenges, and focus greater attention on women’s rights and gender equality. The state of women’s health and nutrition is critical to their overall well-being. Adequate nutritional status of women significantly impacts their work capacity and the health of their children. Eating a well-balanced diet and practicing good nutritional habits can aid in the prevention of several ailments, and thus help in maintenance of good health. In this article, we discuss some of the major nutritional disorders prevalent among Indian women, nutritional needs of women during different life stages, and some tips to address these concerns.

Richa Pande

According to the NFHS 5 data, more than 50 % Indian women and adolescent girls are anaemic. There’s high prevalence of malnutrition concerns like underweight and overweight/obesity at the same time. Additionally, the prevalence on non-communicable diseases (NCDs) like hypertension, diabetes, cancer, heart disease, arthritis, and osteoporosis among Indian women.

They also struggle with micronutrient deficiencies. The above data gives us an insight about the nutritional status of Indian women.

The above data gives us an insight about the nutritional status of Indian women. Now lets us try to understand the reasons behind it. Women are more likely than men to experience nutritional deficiencies due to a variety of factors, including their reproductive biology, low social status, poverty, and lack of education.

Women have different nutritional needs at different stages of life. Women go through several hormonal changes throughout their lives, making certain nutrients essential at different stages for their healthy development and overall well-being.

During adolescence a girl goes through many physical and hormonal changes coupled with increased growth rate, hence nutritious food is essential for her growth and development. Her diet must include all essential macro and micronutrients with an emphasis on adequate consumption of Protein, Calcium, and Iron. Consumption of junk food should be limited. It’s important to practice healthy eating habits during this stage as these will be carried on into later stages of life.

Post adolescence, women undergo a transformative stage as well as these are the years when they pursue higher education, career interests, get married, and plan a family. It’s natural to get stressed during this stage but it’s important to deliberately make good health choices such as staying physically active, taking care of your mental health, avoiding emotional eating, etc. It’s important to have enough amounts of Protein, Iron, Calcium, Vitamin D, Omega -3 fats, and Vitamin B12.

It’s crucial for a woman to have a good nutritional status if she is planning to get pregnant. Women diagnosed with PCOD, thyroid, or anaemia must take special care of their health especially if they are planning to get pregnant. Underweight and overweight women should also focus on weight management before conceiving a child. You can seek a nutritionist/ health practitioner’s advice to manage your diet if you are planning to get pregnant. It’s important to understand that pregnancy can affect your mental health. Also, you can deal with post-partum depression, thus it is advisable to stay educated about mental health and take necessary precautions before pregnancy itself. Know that to deal with the changes during this stage, you need a strong body and mind, which can only be obtained by adopting a healthy eating style, sufficient physical activity, and adequate rest.

During pregnancy, it’s important to seek the advice of a health practitioner and follow it. Take proper rest and adequate sleep. Have foods rich in folic acid, Vitamin B12, Vitamin D, Calcium, Omega-3 fats and Iron. If you face any discomfort, discuss it with your healthcare provider. It’s also important to educate yourself about feeding your child in advance. It’s also important to have knowledge about your nutritional needs when you are feeding your child. You can discuss this with a nutritionist or a dietitian and can further self-educate yourself about it via literature recommended by your health practitioner. Note that along with the nutrients, your fluid intake will play an important role in managing the feeding experience.

It’s important to take care of your health throughout your life but special emphasis must be put on it when you are in your late thirties and early forties. Educating yourself about perimenopause, and menopause is a good idea. Women start perimenopause at different ages. During this stage, you might notice some irregularity in your periods. You are diagnosed to have menopause once you’ve gone through 12 consecutive months without a menstrual period. It’s important to have regular health check-ups during this stage, eating healthy, staying physically active, and taking proper rest and adequate sleep. Practicing yoga, meditation, and breathing exercises can be soothing. It’s vital to have foods rich in Calcium, Folic acid, Vitamin B12, Vitamin C, and Fibre. It’s important to note that post menopause, your body requirement of Iron decreases. If you were taking Iron supplements before menopause, consult your health practitioner for an adjusted dose for during perimenopause and post-menopause.

|

Dietary sources of some micronutrients crucial for women’s health |

|

|

Calcium |

Cereals and legumes like ragi, bengal gram, horse gram, rajma and soyabean). Green leafy vegetables like amaranth, cauliflower greens, curry leaves, knol-khol leave, agathi leaves, Colocasia leaves. Nuts and oilseeds like almonds, sesame seeds, tahini seeds, etc. Dairy products like milk, curd, yogurt, buttermilk, cheese, etc. |

|

Iron |

Green leafy vegetables such as amaranth, spinach, bengal gram leaves, cauliflower greens and radish leaves. Organ meats, poultry, and seafood. Oilseeds like pumpkin seeds, flax seeds, and sunflower seeds. Fortified Salt. Eating iron rich foods with foods rich in Vitamin C improves the absorption of iron. |

|

Vitamin B9/ Folate/ Folic Acid |

Vegetables such as broccoli, amaranth, beets, peas, kale, spinach, etc. Pulses like chickpeas, bengal gram, black gram, green gram, and red gram. Oil seeds like peanuts, sesame seeds and sunflower seeds. Eggs are also a good source of vitamin B9.Citrus fruits like oranges, grapefruit, lemons, and limes are rich in folic acid. Papayas, Bananas, Avocados ARE ALSO RICH IN FOLATE. |

|

Vitamin C |

amla, guava, kiwis, lemons, oranges, papaya, strawberries, tomatoes , |

|

Vitamin D |

egg yolk, salmon, tuna, cod liver oil, sardines, mushroom, Vitamin D fortified foods |

It’s time for women to prioritise their own nutritional and health needs because taking care of ourselves comes before taking care of others. Women frequently disregard these needs. They must also ask for assistance when they need it rather than struggling silently and letting it affect their wellbeing.

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Solar panels are increasingly being installed by homeowners wishing to take advantage of a system that produces green energy and insulates them from rising energy prices. A rooftop solar power system can provide us with a clean and efficient source of energy for the home, saving us money and reducing dependence on the power grid. If you are worried about the amount of money spent in installation, just know that it will pay you back in just six to nine years in terms of savings in monthly bills. The useful life of a typical solar power plant is considered to be 25 years. By choosing solar, you make an investment you can be proud of and show your commitment to clean, renewable energy. In this report, we explain the common types of solar electric systems, the parameters on the basis of which one may choose the one that best suits their requirements, and other points that may concern the consumer.

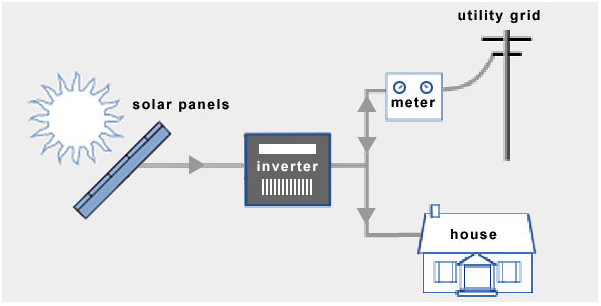

Simply put, a solar rooftop photovoltaic (PV) system converts sun’s light energy into electricity energy through solar panels mounted on the rooftop of a building. This is how a solar panel works. As light hits the solar panels, the solar radiation is converted into direct current (DC). The direct current flows from the panels and is converted by the solar inverter into alternating current (AC) used by local electric utilities. The plant can be connected to the grid or can be designed to be off-grid.

Rooftop solar is helping consumers not only reduce their electricity bills, but also do their bit for the environment. It allows them to generate electricity for self-consumption and sell surplus, if any, to the discom, which in-turn pays them for the surplus energy generated over and above their own consumption as per applicable regulations.

Components that are required for rooftop solar installations are: photovoltaic panels (to convert solar sunshine into direct electricity), batteries to store electricity when power is not required and the sun is shining, inverters to convert direct current (DC) into AC, cables and other miscellaneous items like junction boxes, earthing, lighting arrestors and conduits. Panels account for about 50 per cent of the total cost.

The common types of solar electric system are described here. Each has distinct applications and components.

In this system the solar panels are connected to your local utility electrical grid. A grid-connected system consists of:

Very similar to the grid-connected system, this system adds a battery bank to collect the power generated from the solar panels. Power stored in the batteries can be used during outages. The battery bank collects power produced by the solar panels, sends it to breaker box, and then into the house power system.

Off-grid systems are not tied to any utility power lines and are most common in remote areas where connecting to the utility grid is more expensive than purchasing an off-grid system. In off-grid systems, the solar electric system represents the home’s main source of power. Batteries store unused solar energy for use at night. Generators and other backup fuel sources are sometimes used as backup power when the solar power stored in the batteries is not enough to meet household needs.

Your home’s power requirements, roof type and solar resource will determine the type and size of the solar electric system. The right choice will depend on how much sunlight your area receives, your budget, how much conventional power you want to offset with solar power, and where the solar panels will be mounted. Please check all details at link given below: https://solarrooftop.gov.in/rooftop_calculator

Efficiency is an important parameter. This is a measure of the panel’s electricity output (in watts) compared to its surface area – basically how much solar energy is converted into electrical power, which is usually around 15 per cent to 20 per cent depending upon the sophistication of the panel. Generally, the higher the efficiency, the more power you can get from a given roof area, and you might have lower installation costs too. However, if you have plenty of roof space, you may find it more economical to buy cheaper panels with lower efficiency and just use more of them.

Tata Solar, Luminous Solar, Adani solar, Vikram solar, Moser Baer Solar, Sukam Solar, Havells Solar Solaredge, Microtek Solar, Exide Solar, Waaree Solar, Vikram Solar, Jakson Solar, Lubi Solar, Delta Solar Inverter, ABB Solar Inverter, Consul Neowatt Solar Hybrid Inverters.

The cost of a solar PV system will depend on many variables including the system size and the quality of components used. The approximate cost of a 1 kWp (kilowatt peak) rooftop solar PV project ranges from Rs 55,000 to Rs 85,000 for the state of Delhi – this includes installation charges but excludes cost of storage batteries (if required) and subsidy. The overall cost depends on the size of the project as rates are a little lower for a higher-size project. Prices of solar PV systems offered by various vendors can differ significantly.

Solar PV module (250 watt peak [wp] x 4 [number of systems]): Rs 35,000–Rs 40000/-

PV module mounting structure (1 kW set): Rs 5,000

Tubular batteries (150 Ah x 2 [number of batteries]): Rs 22,000–Rs 28,000

Solar inverter (1.5 kilo-volt-amperes [KVA]): Rs 22,000–Rs 25,000

Cabling and other accessories: Rs 10,000

Transportation and installation: Rs 10,000

The above-mentioned costs will come with GST extra

Generating units per day = 4–4.5 units

(Total project cost of one off-grid rooftop solar system works out to Rs 60,000–Rs 90,000/kWp. Final cost will vary depending on quality of equipments/brands.)

According to solar power system experts, one kilowatt (kw) of the solar system is sufficient for an average family of three to four people with only requirement of running a couple of tube lights, charger and fans. However, for a larger family or to run an air conditioner at home, a 3-5 kW solar system will be required at least.

There is a subsidy of 40 per cent (up to 3 KW) of maximum of the actual project cost from the ministry of new and renewable energy (MNRE), to be routed through discoms.

The consumer can download the solar net-metering rooftop application form from the websites of DISCOMs. The consumer will receive a net import/export bill indicating either net export to the grid or net import from the grid. The consumer will settle the same as per existing norms.

The consumer shall be paid for net energy credits that remain unadjusted at the end of the financial year at the rate of average power purchase cost (APPC) of the distribution licensee for the respective year on provisional basis. The consumer shall settle the same as per existing norms. Discom will pay the consumer for surplus power generated which remain unadjusted at the end of financial year as per existing regulation.

In net metering, the excess solar energy is exported to the grid. This excess solar energy is deducted from the energy imported from the grid subject to certain conditions. The consumer pays for the net energy imported from the grid.

Most solar electric systems come with a five-year guarantee and 25-year warranty, but maintenance may be required to comply with a manufacturer’s warranty.

Proper maintenance of your system will keep it running smoothly. Most vendors recommend a yearly maintenance check by your installer. Solar panel may need to be cleaned in climates with infrequent rainfall.

In grid-connected rooftop, the DC power generated from the solar photovoltaic (SPV) panel is converted into AC power using a power conditioning unit (PCU) and it is fed to the grid, either of 33 kV/11 kV three-phase lines or of 440 volt/220 volt three-phase lines/single-phase line, depending on the capacity of the system installed at institution/commercial establishment or residential complex and the regulatory framework specified for respective states. These SPV systems generate power during the daytime which is utilised fully by powering captive loads and feed excess power to the grid. Where solar power is not sufficient due to cloud cover, etc., the captive loads are served by drawing power from the grid.

Such SPV systems can be installed at the rooftops of residential and commercial complexes, housing societies, community centres, government organisations, private institutions, etc.

A 1 kW rooftop system generally requires 12 sq. metres (130 square feet) of flat, shadow-free area (preferably south-facing). Actual sizing depends also on local factors of solar radiation and weather conditions and shape of the roof.

You need to install the system through a state nodal agency or an MNRE-empanelled agency (that is, contractor) for getting MNRE subsidy.

The usual benchmark for energy generated from a 1 kW solar power plant is 1,500 units per annum. The amount of actual energy generated depends on both internal and external factors. External factors that are beyond the control of a solar power developer can include these:

NIC has developed a simple but informative and useful application for the layman as well as the developers of solar power. Initially android version of the app has developed. The app namely ARUN (Atal Rooftop solar User Navigator) has got the following features.

Ministry of New and Renewable Energy, Government of India is implementing Grid-connected Rooftop Solar Scheme (Phase-II). Under this scheme Ministry is providing 40% subsidy for the first 3 kW and 20% subsidy beyond 3 kW and up to 10 kW. The scheme is being implemented in the states by local Electricity Distribution Companies (DISCOMs).

Residential consumers willing to set-up a rooftop solar plant under MNRE scheme can apply online and get rooftop solar plants installed by listed vendors. For this, they have to pay the cost of rooftop solar plant by reducing the subsidy amount given by the Ministry as per the prescribed rate to the vendor. The process of which is given on the online portal of the DISCOMs. The subsidy amount will be provided to the vendors by the Ministry through the DISCOMs. Domestic consumers are informed that to get subsidy under the scheme of the Ministry, they should install rooftop solar plants only from the empanelled vendors of the DISCOMs following due process of approval by DISCOMs.

For more information, contact the concerned DISCOM or dial MNRE’s toll free number 1800- 180-3333. Click on https://solarrooftop.gov.in/grid_others/discomPortalLinks to know the online portal of your DISCOM.

Sources: http://mnre.gov.in, https://solarrooftop.gov.in

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

We are presenting to you the top 10 judgements of the year 2022. This is the second part. This part has five summarised judgements. To read the full case and judgments, please subscribe to our buying guide for the details. You can find it in ‘Top 10 Judgements-2022’.

Dr Prem Lata, Legal Head VOICE

Civil Appeal No. 6943 of 2021/ Decided February 21, 2022

Head Note-The matter cannot be left unresolved because an unnecessary party was added. An unneeded party may be struck down by the court.

The National Consumer Disputes Redressal Commission issued an order on September 27, 2021, by which the complaint was returned unadjudicated for the reason that the surveyor was an unnecessary party in the insurance claim dispute. These facts served as the basis for the appeal before the SC. The claimant or appellant was granted the right to submit a new complaint within 30 days. The insurance company was to be the “sole opposite party for pursuing reparation” while being granted freedom.

Civil appeal No. 3778 of 2020/ Decided March 03, 2022

Head Note- Corporate Insolvency Resolution Process (CIRP) proceedings against a builder can be withdrawn if parties settle the issue

In the case of Amit Katyal Vs Meera Ahuja & others, home buyers in the housing project Krrish Provence Estate at Gurgaon had gone against Jasmine Buildmart Pvt. and invoked Section 7 of IBC 2016 before the Adjudicating Authority/NCLT.

But later, the original applicants filed IA No. 18679 of 2022 under Article 142 of the Indian Constitution and Rules 11 and 12 of the National Company Law Tribunal Rules, 2016, requesting permission to end the CIRP proceedings upon receiving payment of Rs. 3, 36, 02,000/- plus applicable interest from the money the appellant had deposited in the registry of this court.

Civil appeal No 6730 of 2010/ Decided on March 24, 2022

Head Note-Selling Repainted & Repaired vehicles, deficiency of services

Complaint before District Forum Gurgaon under CP Act 1986

Civil Appeal No. 6044 of 2019 with Civil Appeal No. 7149 of 2019/ Decided on April 07, 2022

Head Note- SC allowed three fold choices to the home buyer, not been given possession of dwelling within stipulated time

In a case resolved on April 7, 2022, the SC adopts a very lenient stance in favour of homebuyers who put their hard-earned money into a developer’s project but did not receive possession by the deadline.

SLP (Civil) 19374/2021/Decided on April 22, 2022

Head Note –Speech during Parliament debate is of little relevance

SC Re-affirms its stand on Healthcare service under Consumer law

An organization “Medicos Legal Action Group” had filed a writ petition before the High Court of Bombay as Public Interest Litigation No. 58 of 2021 and prayed before the court to declare that services performed by healthcare service providers are not included within the purview of the Consumer Protection Act 2019.